Table Of Content

Mortgage loan terms can vary, but most borrowers choose either a fixed-rate 15-year or 30-year mortgage. You can adjust your monthly mortgage payment by changing the loan terms. To figure out how much home you can afford with our calculator, enter your gross annual income and total monthly debts, choose a down payment amount and select a loan term. Homeowner's insurance is based on the home price, and is expressed as an annual premium.

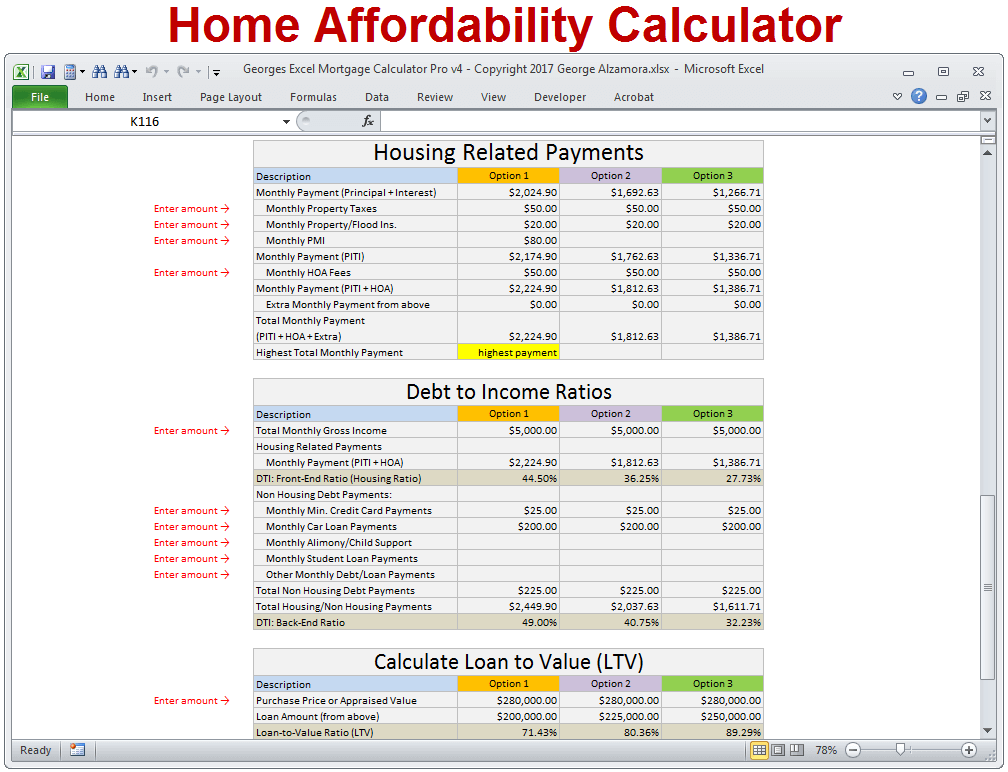

House affordability based on fixed, monthly budgets

Having less debt can improve your credit score and increase your monthly cash flow. Alternatively, a refinance calculator can help you decide whether or not refinancing your current mortgage loan will result in a lower monthly payment. We’ll check your credit history to give you an even more solid estimate of what you can afford, along with your expected rate and monthly payment. This loan is a great option for anyone who is a veteran or currently serving in the United States military. The loan does not require any down payment, and unlike other loans, it also does not require private mortgage insurance. Adjustable-rate mortgages (ARMs) have interest rates that can change over time.

Loan Estimate

After all, deferment and forbearance only grant borrowers a short-term reprieve—much shorter than your mortgage term will be. A mortgage calculator can be helpful when estimating your home buying budget. But remember — even if you can afford the monthly payments, you still need to qualify for a home loan. When lenders assess whether or not you can afford a mortgage loan, they’ll compare your estimated PITI with your gross monthly income (income before taxes and deductions).

Mortgage options and terminology

Multiple mortgage brokers said they find lenders will generally approve you for conforming loans if your debt-to-income ratio doesn’t exceed 45%. If you are looking to buy a house that requires a mortgage above these caps, you’ll need to take out something called a jumbo loan. You can still use the calculator to get a sense of what you might be able to afford, though it will be less accurate. Hopeful homeowners have a number of agencies to turn to in California.

Get Accurate, Real-Time Rates With Rocket Mortgage®

Lenders have maximum DTIs in place that could stand in the way of getting approved for a mortgage. On conventional loans, for example, lenders usually like to see debt-to-income ratios under 36 percent. Most are willing to go up to 43 percent, and in some cases, 50 percent is the cutoff. Depending on how much you change the home price in the mortgage calculator, it could drastically change your estimated monthly mortgage payments. You can play around with those numbers a little to figure out what kind of monthly payment you can afford.

Mortgage Preapprovals Vs. Prequalifications: Which Should You Get?

How Much House Can I Afford On a $125K Salary? - Yahoo Finance

How Much House Can I Afford On a $125K Salary?.

Posted: Tue, 30 May 2023 07:00:00 GMT [source]

The problem is that some people believe the answer to “How much house can I afford with my salary? ” is the same as the answer to “What size mortgage do I qualify for? ” What a bank (or other lender) is willing to lend you is definitely important to know as you begin house hunting. You have to make the mortgage payments each month and live on the remainder of your income.

What Does A Mortgage Payment Include?

Mortgage Prequalification Calculator – Forbes Advisor - Forbes

Mortgage Prequalification Calculator – Forbes Advisor.

Posted: Mon, 21 Aug 2023 07:00:00 GMT [source]

If you’re moving from Portland, Oregon to sunnier San Diego, you’ll see a 9% increase in your cost of living on average. Some of the major considerations of owning property in California other than price is earthquake risk, drought and wildfire. Despite the relatively frequent occurrence of natural disasters, including wildfires and earthquakes, the state has lower insurance costs than half of the nation. The average annual policy is about $1,027 a year, according to Insurance.com data.

Find out how much of a mortgage you can qualify for and how much house you can afford

A high DTI commits much of your household income to housing payments. Homeowners insurance should not be confused with private mortgage insurance, which is something else entirely. If you obtain home financing, you’ll repay more than the amount you borrowed because the amount you repay is determined by several factors, including the interest and loan amount. List out your expenses and then add them together to get your total monthly spending.

Remember that there are other major financial goals to consider, too, and you want to live within your means. Just because a lender offers you a preapproval for a large amount of money, that doesn’t mean you should spend that much for your home. One of the costs you’ll want to consider during the home-buying process is a home inspection. Before you close the deal on a house, there’s usually a period where you can arrange a home inspection to determine the state of the house and any potential problems with the property. If problems are found, you generally have some negotiating power over the seller for repairs or price. Typical costs range from $200 to $500, with larger houses falling on the higher end of the price range.

Other homes are in locations where lenders will not require you to buy flood insurance. However, you might want to purchase it anyway after investigating the area’s flood risks. You can get a flood insurance quote from the National Flood Insurance Program, but private insurers may be able to offer a better deal. Expect to pay mortgage insurance premiums for at least a few years. They’ll cost 0.17% to 1.86% per year per $100,000 you borrow, or $35 to $372 per month on a $250,000 loan. Homeowners insurance costs more in places where homeowners file more claims.

Click "Amortization" to see how the principal balance, principal paid (equity) and total interest paid change year by year. Using the Rocket Mortgage calculator is a good way to get started. This calculator can help you determine the type of home you can afford.

If you're purchasing, the appraised value usually needs to be equal to or greater than the home's purchase price. Our calculator is preset to a “conservative” 28% DTI ratio; most lenders set a maximum DTI limit between 41% and 45%. You can slide the bar up to an “aggressive” 50% DTI ratio if you’re willing to make room in your budget for a higher payment. Here are a few documents you should gather to help you understand your financial situation and how much house you can afford. This information will also be required when you apply for a pre-approved home loan. Generally, the higher the credit score you have, the lower the interest rate you’ll qualify for and improve overall what you can afford in a home.

When you’re ready, your home mortgage consultant will help you complete an application. It takes only a few minutes, and there is no impact to your credit score. Get informed about the mortgage and homebuying process, from starting your home search to planning your next move. Financial planners often mention the “28/36 rule” when it comes to home affordability. The higher your down payment, the higher the loan amount you can qualify for. Perhaps more importantly, however, you avoid putting yourself at the limits of your financial resources if you choose a house with a price lower than your maximum.

Bankrate’s mortgage calculator can help you explore how different purchase prices, interest rates and minimum down payment amounts impact your monthly payments. And don’t forget to think about the potential for mortgage insurance premiums to impact your budget. If you make a down payment of less than 20 percent on a conventional loan, you’ll need to pay for private mortgage insurance, or PMI. For most borrowers, the total monthly payment sent to your mortgage lender includes other costs, such as homeowner's insurance and taxes.

Lenders take into account the share of your income that goes toward paying debt — or your debt-to-income ratio — when determining whether you can afford a mortgage. Qualified mortgages, which are mortgages designed to improve the chances that borrowers can pay them back, usually require a debt-to-income ratio below a maximum percentage. If your mortgage loan is backed by the Federal Housing Administration (FHA), you’ll have the added expense of up-front mortgage insurance and monthly mortgage insurance premiums. The calculator doesn’t display your debt-to-income (DTI) ratio, but lenders care a lot about this number. They don’t want you to be overextended and unable to make your mortgage payments. After you close, your mortgage loan servicer will deposit part of your total monthly payment into another escrow account.

Thanks for the detailed post on USDA loans! It's great to see more information on this lesser-known but incredibly helpful option for homebuyers. Usda Home Loan is a fantastic choice for those looking to buy in rural with the zero down payment benefit. Looking forward to more insight like this!

ReplyDelete